We all know the importance of saving for an emergency. Putting aside money for unexpected expenses helps protect against missed payments or racking up unnecessary credit card debt. But, creating an emergency savings isn’t always as easy as it seems.

Those of us on a tight budget may struggle with where to pull the savings from. Putting aside money each week often means going without in another aspect.

How much should I have in emergency savings? Everywhere you turn, the answer is 3-6 months worth of salary / expenses. THREE TO SIX MONTHS?! How can I come up with that kind of money if I can’t even cover 3-6 weeks?…. errr, even 3-6 days?

Despite many attempts at saving for an emergency, it’s never felt like enough. I once got a few hundred dollars saved up only to spend it — because why did it even matter? The amount saved was practically nothing, as it was much closer to zero than the thousands I needed to meet the suggested nest egg.

Does this sound familiar?

The $20 Emergency Fund

One of my favorite money reads of all time is called The $20 Emergency Fund. I first came across this article in 2017 and it changed my entire perspective on savings. The basis of the article is that you can’t get to a $10,000 goal by staying at zero. But, you can get closer by putting aside $20, $10 or even $1.

Upon reading, I immediately opened a separate emergency savings goal account. I started by setting up a recurring transfer each week of $5. Prior to this, I was having a hard time putting aside $20 without dipping into it, but $5 was manageable. I continued this auto transfer until $5 seemed negligible. Then, I bumped it up to $10, $20 and eventually $25.

What I discovered through this process was two things: 1) the power of micro goals and 2) the importance of building sustainable habits.

Setting Micro Goals

How was I ever going to get to $10,000 if I spent the greater part of 10 years trying to make it to $1,000?

Saving up $200 out of $10,000 felt like nothing. But, saving $200 out of $200 (and not touching it) was a HUGE accomplishment for me! Trying to sock away $100/week to accelerate the savings felt like a tortoise and hare situation. I’d go strong out of the gate and make it three weeks at $100/week, but would be sacrificing everything else. This would lead to a loss, where I would wipe out the entire amount saved.

I found that slow and steady was the way to go. Breaking this down into smaller goals was a game changer! Could I successfully save $100 without touching it? $200? ….dare I say, $500! Each tortoise-like milestone increased confidence and helped build momentum. Sometimes micro goals didn’t come in dollars but in time passed or moments of savings. Even $5/week, successfully saving for 5 weeks felt like an unstoppable streak! I did something successfully for 35 whole days; a total of 50,400 impeccable minutes of savings!

The idea of setting micro goals can actually be applied to any area of your life:

- Feel like your house is too cluttered? Start by getting rid of one item per day.

- Want to grow your professional network? Focus on building relationships by connecting with one new person per week on LinkedIn.

- Wish you were a better cook? Practice one new recipe a month.

Building Sustainable Habits

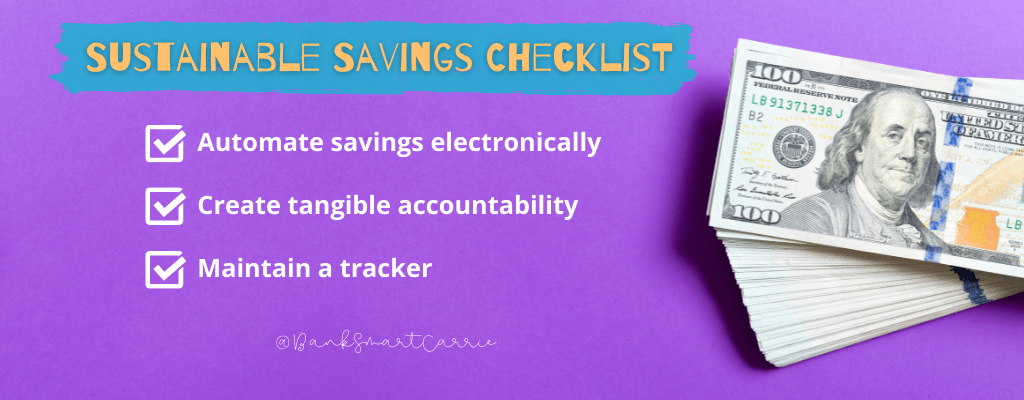

The next thing I learned is that it was never about an exact amount of money. How could I ever save $100/week if I hadn’t even managed to save $1? It just wasn’t second nature. I wasn’t in the habit of saving. I needed to build a sustainable savings routine, which I was able to do with three key steps:

- Automate savings electronically – Setting up recurring savings transfers helped to build it into my weekly routine. Keeping the amounts manageable allowed me to maintain the habit. I have since been able to increase the dollar amount and add additional recurring transfers with minimal effort.

- Create tangible accountability – At one point I felt like I hit a savings plateau. Although I had been able to maintain my emergency savings habit, I wasn’t able to prioritize saving for other goals (or concurrently, reducing expenses to reallocate savings). In an attempt to move forward, I started participating in savings challenges with a bestie. This gave me an accountability partner to check in with. Because we used cash to make it tangible, I got creative and started posting my weekly savings on Instagram stories. This eventually became a welcomed habit, part of my weekly routine and something I looked forward to.

- Maintain a tracker – We often think about tracking habits we want to break. When I wanted to quit drinking caffeine, I began using a simple app called Quit That!, which tracked the time since my last sip down to the second. I’ve since maintained a successful streak of over 1,000 days. Most times, the only thing that kept me from cracking open an energy drink was the fact that I didn’t want to break my streak. What if we applied that same concept to savings, keeping track of # of days saved? Using a tracker – whether it’s an app or good old fashioned paper tally marks – helps to build a streak worth maintaining.

Macro Success

I’m proud to share that at the beginning of this year I hit $5,000 in my emergency fund! While it’s still not 3-6 months of expenses, it’s a whole lot closer! And it has come in handy, saving me from a few unexpected mishaps along the way.

For someone who not that long ago couldn’t maintain $500 in a savings account to save her life; this is a HUGE win. Each win big or small has helped to build confidence and momentum and it all started with micro goals.

If you’re ready, let’s get saving!

This post is written for America Saves Week! ASW is an annual celebration as well as a call to action for everyday Americans to commit to saving successfully. Join the discussion at #ASW2022 and let’s get saving!